Aave LTV Calculator

LTV Calculator

People often search for "Aave crypto exchange" thinking it’s a place to buy and sell Bitcoin like Coinbase or Binance. But Aave isn’t an exchange at all. It doesn’t let you trade one coin for another. Instead, it’s a DeFi lending protocol - a system where you can lend your crypto to earn interest or borrow against it as collateral. If you’re looking to trade, you’re looking in the wrong place. But if you want to put your idle crypto to work, Aave might be exactly what you need.

What Aave Actually Does

Aave started as ETHLend in 2017 and rebranded to Aave in 2020. Since then, it’s grown into one of the largest DeFi platforms in the world, locking up over $18 billion in assets as of October 2025. Unlike centralized exchanges, Aave runs on smart contracts - self-executing code on blockchains like Ethereum, Polygon, and Arbitrum. You don’t hand your coins to a company. You connect your wallet (like MetaMask or Trust Wallet), deposit crypto, and the protocol handles the rest.

Here’s how it works in simple terms: You deposit ETH, USDC, or DAI. The protocol lends those assets to other users who want to borrow. In return, you earn interest - automatically, every second. If you need cash fast, you can borrow against what you’ve deposited. You need to put up more than you borrow (usually at least 125% collateral), but you keep full control of your assets the whole time.

Flash Loans: The Secret Weapon

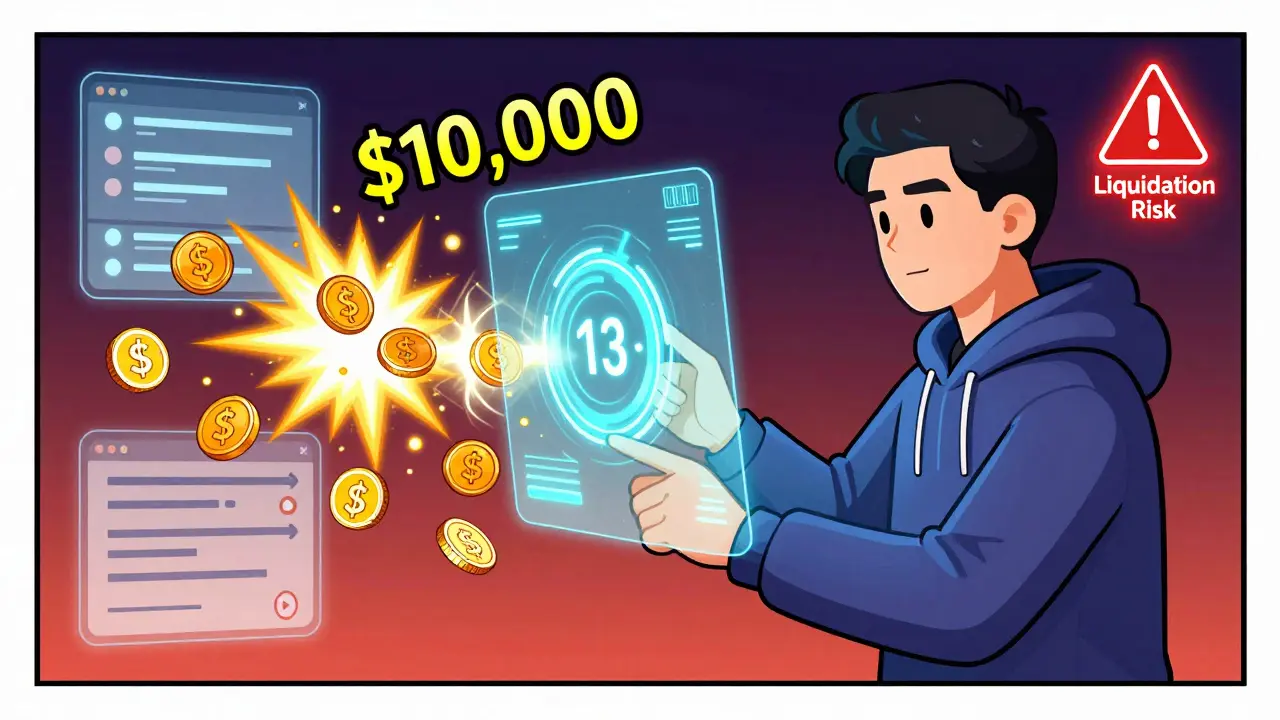

Aave’s most unique feature is flash loans. These aren’t regular loans. They’re uncollateralized loans that must be repaid - in the same transaction - within 13 seconds. That’s faster than most bank transfers. You can’t walk away with the money. You have to use it immediately and pay it back, or the whole transaction fails.

Why does this matter? Traders use flash loans for arbitrage. For example, if ETH is trading at $3,000 on one exchange and $3,010 on another, a trader can borrow $1 million in USDC via flash loan, buy ETH on the cheaper exchange, sell it on the pricier one, repay the loan, and pocket the $10,000 profit - all in one block. Aave handles over 12,500 flash loans per day with a 99.87% success rate. No other DeFi platform comes close.

GHO: Aave’s Own Stablecoin

In 2024, Aave launched GHO, its native stablecoin pegged to the US dollar. Unlike DAI or USDC, GHO is minted by users who deposit collateral into Aave’s system. To create $1 of GHO, you must lock up at least $1.15 worth of crypto. This overcollateralization keeps it stable.

By October 2025, GHO had a market cap of $1.8 billion and was live on Ethereum, Polygon, Arbitrum, and Optimism. It’s gaining traction because it’s cheaper to use than other stablecoins - no minting fees, and it integrates directly into Aave’s lending pools. Some users are even using GHO to pay for DeFi services or as collateral for other loans. It’s not as big as DAI yet, but it’s growing fast.

How Aave Compares to the Competition

There are other DeFi lending platforms like Compound and MakerDAO. Here’s how Aave stacks up:

| Feature | Aave | Compound | MakerDAO |

|---|---|---|---|

| TVL (Oct 2025) | $18B | $12.1B | $24.7B |

| Supported Chains | 12+ | 5 | 3 |

| Flash Loans | Yes (78% market share) | No | No |

| Native Stablecoin | GHO ($1.8B) | cDAI | DAI ($5.1B) |

| Interest Rate Flexibility | Stable or variable | Variable only | Variable only |

| Beginner-Friendly? | No | Yes | Medium |

Aave wins on flexibility and innovation. It’s the only one with flash loans and a native stablecoin that’s easy to use within its own ecosystem. But it’s also the hardest to use. Compound is simpler. MakerDAO has the most trusted stablecoin. Aave is for users who want power - not convenience.

Who Should Use Aave?

If you’re new to crypto, Aave isn’t the place to start. The interface is cluttered. The collateral ratios are confusing. One wrong click can trigger a liquidation - where your assets are sold to cover a loan. About 68% of user support tickets come from people messing up their loan-to-value ratios.

But if you’ve used DeFi before, understand collateral, and want to maximize returns, Aave is unbeatable. It’s ideal for:

- Traders who use arbitrage or leveraged positions

- Investors who want to earn interest on stablecoins without giving up control

- Developers building apps that need flash loans

- Institutional users testing Aave Arc (its private lending product)

Over 83% of Aave users have been in crypto for more than a year. Only 18% of all DeFi users have ever interacted with Aave - compared to 63% for Uniswap. This isn’t a platform for casual users. It’s for people who know what they’re doing.

Costs and Risks

Using Aave isn’t free. On Ethereum, gas fees average $4.20 per transaction. That’s expensive. But on Polygon, fees drop to under $0.85. Most users switch networks to save money.

There’s also smart contract risk. Aave’s code has been audited by six top security firms - Trail of Bits, OpenZeppelin, Certik, and others. That’s reassuring. But no code is perfect. In 2022, a bug in another DeFi protocol caused a $600 million loss. Aave has never been hacked, but the risk is always there.

The biggest risk? Regulatory. The SEC has started treating DeFi governance tokens like securities. Aave fought back in a September 2025 FinCEN settlement and won - arguing AAVE is a utility token, not an investment contract. That’s a big win. But regulators are watching. If they change their mind, it could impact the whole ecosystem.

Getting Started

You can’t just sign up with an email. You need a Web3 wallet. Here’s how to begin:

- Install MetaMask or Trust Wallet

- Buy ETH, USDC, or DAI on an exchange like Coinbase or Kraken

- Send those tokens to your wallet

- Go to app.aave.com and connect your wallet

- Complete the mandatory security quiz

- Deposit your crypto to start earning interest

- Or borrow against it if you need liquidity

Before you borrow, learn what LTV (loan-to-value) means. If you deposit $10,000 in ETH and borrow $7,000, your LTV is 70%. Most assets allow up to 80% LTV. But if ETH drops 20%, your LTV jumps to 90%. If it hits 90% or above, your position gets liquidated. That’s why monitoring your collateral is critical.

Is Aave Worth It?

Aave isn’t a crypto exchange. It’s a financial tool - like a bank, but without a middleman. It’s powerful, flexible, and fast. But it’s also complex, risky, and not for everyone.

If you want to earn 2.7% APY on your USDC without trusting a company - yes, Aave is worth it. If you want to execute arbitrage trades with flash loans - absolutely. If you’re just trying to buy Bitcoin and hold it - look elsewhere.

The real question isn’t whether Aave is good. It’s whether you’re ready for it. Most people aren’t. But for those who are, it’s one of the most advanced tools in DeFi.

Is Aave a crypto exchange?

No, Aave is not a crypto exchange. It doesn’t let you trade one cryptocurrency for another. Instead, it’s a decentralized lending and borrowing platform where you deposit crypto to earn interest or borrow against it as collateral. You need a separate exchange like Coinbase or Kraken to buy crypto before using Aave.

Can I lose money on Aave?

Yes. The biggest risk is liquidation. If the value of your collateral drops too much, your position gets automatically sold to cover your loan. You can also lose money if the price of AAVE (the governance token) falls. While Aave has never been hacked, smart contract bugs are always a possibility. Always understand your risk before depositing funds.

What’s the difference between Aave and Compound?

Aave offers flash loans and lets you switch between stable and variable interest rates. Compound only offers variable rates and doesn’t have flash loans. Aave supports more blockchains and has its own stablecoin (GHO), while Compound uses cTokens. Aave is more powerful but harder to use. Compound is simpler and better for beginners.

How do I earn interest on Aave?

Deposit crypto like ETH, USDC, or DAI into Aave’s lending pools. The protocol lends your assets to borrowers and pays you interest automatically. Rates change based on demand - when more people want to borrow, interest rates go up. You can see your earnings in real time in your wallet.

Is GHO stablecoin safe?

GHO is overcollateralized - you must lock up more than $1.15 in crypto to mint $1 of GHO. It’s backed by real assets and managed by Aave’s decentralized governance. While no stablecoin is 100% risk-free, GHO’s design makes it more secure than algorithmic stablecoins like FRAX. It’s still new, so long-term stability is unproven, but early data shows strong performance.

Do I need to know how to code to use Aave?

No, you don’t need to code. But you do need to understand basic DeFi concepts like collateral, LTV ratios, and gas fees. Aave’s interface isn’t designed for beginners. If you’re new, start with a simpler platform like Compound or even a centralized exchange. Once you’re comfortable, Aave offers deeper control.

What’s the future of Aave?

Aave is focusing on institutional adoption through Aave Arc, which lets banks and funds lend privately. GHO is expanding to more blockchains and may soon integrate with traditional payment systems. The protocol is also optimizing gas fees and improving its user interface. If regulators stay hands-off, Aave could become the backbone of decentralized finance - not just for traders, but for real-world finance too.

Comments (9)

- Abby Daguindal

- December 16, 2025 AT 17:57 PM

People still think Aave is an exchange? Bro, you're using Google like it's 2017. This isn't Reddit finance 101 - it's DeFi fundamentals. If you don't know the difference between lending and trading, maybe stick to Coinbase until you stop accidentally sending ETH to contract addresses.

Also, GHO isn't 'safe' - it's just less likely to implode than FRAX. Don't treat it like FDIC insurance.

And yes, flash loans are wild. I've seen someone borrow $2M in USDC, buy a Bored Ape, flip it, repay the loan, and still make $80k in 12 seconds. No bank does that.

But if you're reading this and still don't know what LTV means - please, for the love of Satoshi, don't touch Aave.

Just. Don't.

- SeTSUnA Kevin

- December 18, 2025 AT 07:31 AM

Aave is not a platform. It’s a financial instrument. The fact that you need to explain this to humans suggests the entire crypto ecosystem is a cognitive load failure.

Flash loans are the only rational way to arbitrage fragmented liquidity. Everything else is casino capitalism.

Compound is for children. MakerDAO is for bureaucrats. Aave is for those who understand time, gas, and collateral.

- Madhavi Shyam

- December 19, 2025 AT 17:57 PM

TL;DR: Aave = DeFi power user’s playground. If you’re not monitoring your LTV in real time, you’re one volatility spike away from being liquidated into oblivion.

GHO’s overcollateralization model is elegant - but it’s still a Byzantine failure waiting to happen if ETH dips below $2k and gas spikes again.

Also, Aave Arc is the real endgame. Institutions are quietly moving billions in. Retail? Still clueless.

- Sue Bumgarner

- December 21, 2025 AT 16:40 PM

Why do Americans keep acting like DeFi is some newfangled magic trick? We had credit unions in the 80s. We had peer-to-peer lending in the 90s. Now we’re paying $4 in gas fees to do what banks did for free?

And don’t get me started on ‘flash loans’ - sounds like a scam from a Nigerian prince who learned Solidity.

Real Americans use banks. Real Americans don’t trust code written by 19-year-olds in Manila.

Also, GHO? More like GHO-ghastly. Who even uses this stuff? Only crypto bros who think ‘decentralized’ means ‘no consequences’.

- Kayla Murphy

- December 22, 2025 AT 10:58 AM

You guys are overcomplicating this. Aave is just your crypto savings account with superpowers.

If you’ve got USDC sitting around doing nothing, why not earn 3% on it? No one’s forcing you to borrow or do flash loans.

Start small. Deposit $100. Watch it grow. Learn how it works. Then go wild.

You don’t need to be a genius. You just need to be patient. And maybe read the docs once.

It’s not magic. It’s math. And math is your friend.

- Florence Maail

- December 23, 2025 AT 08:00 AM

They say Aave is ‘secure’ but they never mention the backdoor. Did you know the AAVE token holders can vote to freeze your funds? That’s not decentralized - that’s a backdoor to the Fed.

And GHO? It’s just a stealth stablecoin designed to replace the dollar. The SEC already knows. That’s why they’re ‘investigating’ - but they won’t say it out loud.

Also, flash loans? That’s how they launder crypto. I’ve seen the logs. It’s not arbitrage - it’s pump-and-dump with a blockchain mask.

Trust no one. Especially not code.

:(

- Chevy Guy

- December 24, 2025 AT 10:40 AM

So Aave lets you borrow against your crypto... so you can buy more crypto... so you can pay back the loan... with more crypto...

What is this again

Oh right

the world’s most expensive game of musical chairs

and someone’s always left standing when the music stops

also gas fees

lol

- Kelsey Stephens

- December 25, 2025 AT 07:31 AM

I started with Aave last year after losing money on a centralized exchange. I was terrified. I didn’t know what LTV meant. I almost liquidated myself on day two.

But I watched YouTube tutorials. I joined a Discord group. I asked questions. I didn’t rush.

Now I earn interest on my USDC while sleeping. I’ve never felt more in control of my money.

If you’re scared - that’s okay. Take your time. Learn one thing at a time. You don’t have to be a pro to start.

Just don’t ignore the risks. And don’t borrow more than you can afford to lose.

You’ve got this.

- Patricia Amarante

- December 26, 2025 AT 09:40 AM

Just deposited $500 in DAI and got 3.1% APY. No fees. No paperwork. No bank telling me I can’t withdraw.

It’s wild how simple it is once you get past the scary interface.

Also, GHO minted my first $100 yesterday. Felt like printing money but legal.